Key takeaways

- National forecast: CBA now expects national home prices to be flat over 2026, down from 3% at the May Budget and 5% in March, even though the tax changes do not start until 1 July 2027.

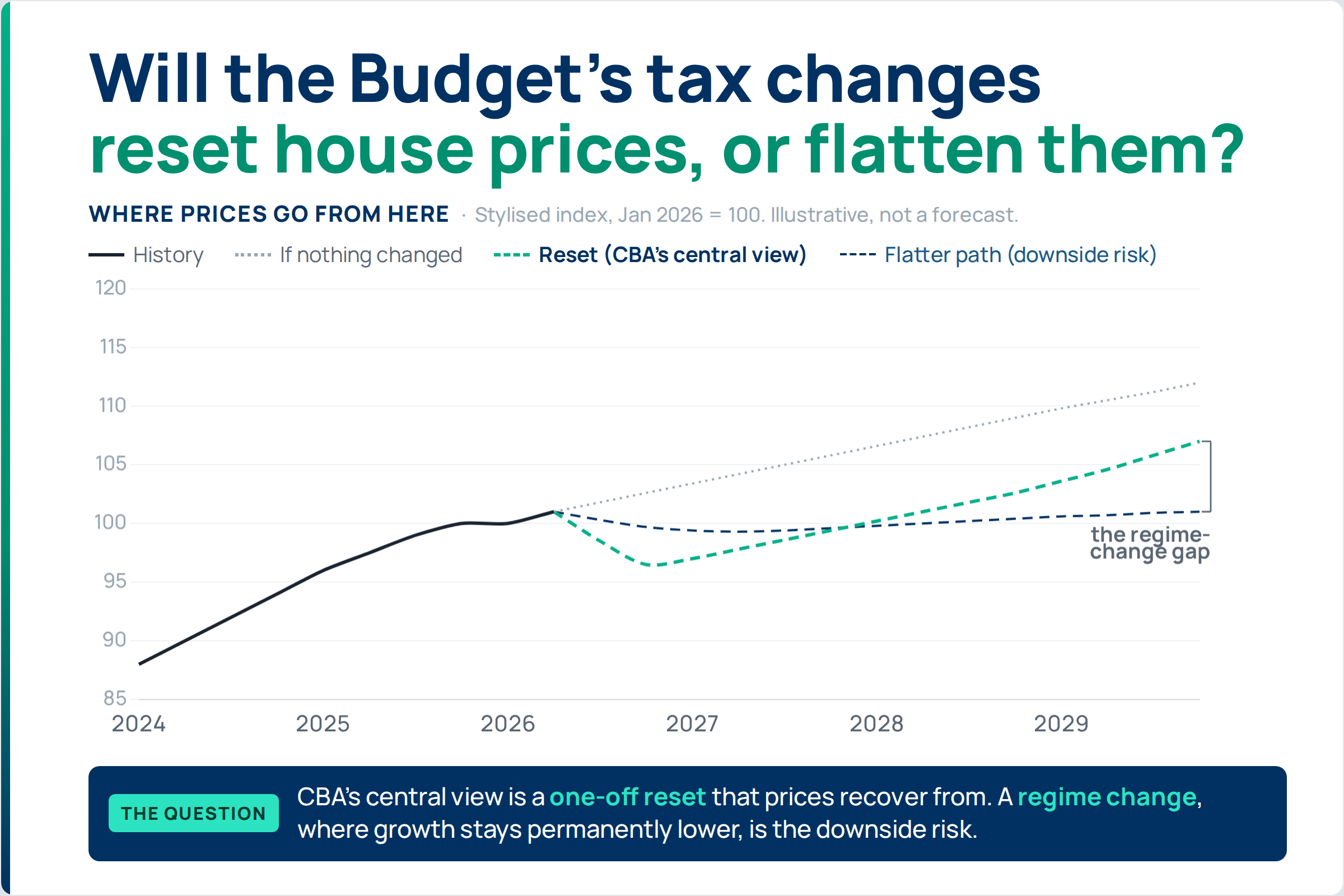

- The question: CBA’s central view, broadly shared by Treasury, is a one-off hit, prices settle about 5% lower, then growth resumes its old path; the risk CBA flags is that weaker investor demand instead holds the growth path permanently flatter.

- Two-speed market: home values to May 2026 show Perth up 25.8% and Brisbane up 19.1% over the year, while Sydney (+2.3%) and Melbourne (+0.5%) are already falling quarter on quarter.

- The maths: to offset the immediate cash-flow hit on a typical Sydney investment, the gross rental yield would need to rise roughly 1.1 to 1.3 percentage points, about three times the 0.4 point the optimistic case assumes.

- Investor signal: the changes bite hardest where investor share is highest and yields lowest, which is Sydney (NSW investor share 43.4%, gross yield 3.2%), not the supply-short capitals leading the market.

What CBA actually changed

Australia’s biggest home lender has cut its house-price forecast twice in three months. Commonwealth Bank now expects national home prices to be flat over the year to December 2026, down from the 3% growth it pencilled in on Budget night in May and 5% back in March.

The reason is a pile-up of headwinds: three interest-rate rises in quick succession, weaker buyer sentiment, homes that are increasingly hard to afford, and the Budget’s changes to how property investors are taxed. Two of those tax changes matter most. The first limits negative gearing to new properties. Negative gearing lets an investor deduct the yearly loss on a rental property, when the rent does not cover the interest and costs, against their other income such as wages, which lowers their tax bill. From 1 July 2027, that deduction will no longer apply to established properties. The second change replaces the 50% capital gains tax discount, the rule that currently taxes an investor on only half the profit when they sell. In its place, the purchase price is lifted for inflation, so only the gain above inflation is taxed, and that gain is taxed at a rate of at least 30%.

Neither change has actually taken effect yet. Both start on 1 July 2027, more than a year away. The slowdown now showing up in the data was already underway before the Budget, driven by rate rises and worsening affordability. CBA’s read is that the tax announcement has so far added to it mainly through weaker sentiment, since actual after-tax cash flows cannot change until the rules do. For reference, Treasury estimated the long-run drag on prices at about 2%; CBA now puts it at just under 5%.

A one-off hit, or a lasting drag?

The whole argument comes down to one question: whether higher rents can eventually refill the hole the tax changes leave in an investor’s return. CBA’s answer is that the effect is a one-off reset. It estimates prices will settle just under 5% below where they would otherwise have been, then resume roughly the same growth path as before. The logic is that once prices are a little lower and rents a little higher, rental yields rise enough to make property attractive again, and investors return with much the same buying power. Prices end up lower, but they keep growing at the same pace as before.

There is a counterargument worth taking seriously, and CBA itself flags a version of it as its downside scenario. The old investor model was built on borrowing heavily against lightly taxed capital gains, propped up by the ability to deduct holding losses each year. The Budget strips out much of both. So the question is not only whether prices step down once, but whether the reason to hold property at all has weakened. The gross rental yield, the annual rent as a share of the property’s value, would have to rise a long way to replace the capital-gains case. If it cannot, investors may simply be willing to pay less for property for good, and that kind of lasting fall in investor demand would mean prices grow more slowly from here, not just dip once.

That is the difference between a reset and a regime change. With a reset, prices drop once and then climb at their old pace. With a regime change, they climb more slowly from here on. CBA is forecasting the first, and it is the better-supported view: its estimate rests on the standard “user cost” approach, where prices and rents adjust until property is worth holding again, and Treasury’s own read of the long-run hit is smaller still, at about 2%. The second, permanently slower growth, is the downside risk CBA itself flags.

The two-speed market is already here

The slowdown is real, but it is not national: our own data shows the split widening, with three capitals surging and two going backwards. The figures below are to 31 May 2026, a month more recent than CBA’s note, and they show a market splitting in two.

Perth is up 25.8% over the year and still rising at 4.8% in the latest quarter. Brisbane is up 19.1%, Adelaide 12.3%, and all three are still climbing. At the other end, Sydney (up just 2.3% over the year) and Melbourne (up 0.5%) have already turned, with both falling more than 2% in the most recent quarter. Canberra is edging down too. The flat national figure is an average of these opposite movements, not a description of any single city.

Where the tax changes bite hardest

The tax changes hit hardest where three things line up: a high investor share of recent lending, a thin rental yield, and a high price. The scorecard below ranks the five largest capitals on all three.

| City | Median value | Annual growth | Quarterly change | Gross yield | Investor share (State)* |

|---|---|---|---|---|---|

| Perth | $1.05m | +25.8% | +4.8% | 3.6% | 39.1% |

| Brisbane | $1.13m | +19.1% | +3.4% | 3.3% | 41.4% |

| Adelaide | $0.95m | +12.3% | +2.8% | 3.4% | 42.5% |

| Sydney | $1.28m | +2.3% | −2.1% | 3.2% | 43.4% |

| Melbourne | $0.81m | +0.5% | −2.3% | 3.9% | 34.6% |

| National | $0.94m | +8.8% | +0.6% | 3.6% | 40.3% |

On all three measures, Sydney is the most exposed to weaker investor demand of any capital. Investors take 43.4% of new mortgage lending in New South Wales, the closest read on Sydney since the lending data is reported by state, and the highest share anywhere. Sydney’s gross yield is the lowest of any capital at 3.2%, on the highest median value at $1.28 million. So Sydney combines the most investor exposure, the thinnest rental cushion, and the most expensive, most heavily borrowed-against stock. If investor demand softens, it shows up here first.

That exposure is real, but two points shape what it means. First, the negative-gearing change does not touch property already owned: anything bought before Budget night keeps its negative gearing. And neither reform starts until 1 July 2027, so for now the effect runs through new investor purchases and buyer confidence, not the deductions current owners already claim. Second, being the most exposed is a ranking on three measures, not a forecast that Sydney prices will fall the furthest. The quarterly falls showing up now are the rate-and-affordability cycle at work, not the tax changes, which have not started. And Sydney’s rents are still rising, up 5.3% over the year to February 2026, which lifts yields the slow way even as prices ease.

Melbourne is exposed too, but for different reasons, and it is worth being precise rather than lumping the two together. Victoria has the lowest investor share of the mainland states at 34.6%, and Melbourne’s yield of 3.9% is healthier than Sydney’s. Melbourne’s weakness owes more to years of soft price growth and weak rents than to investor concentration. The booming capitals sit in the opposite corner: strong growth, tight rentals, and prices supported by demand that has nothing to do with the tax change.

The maths the recovery depends on

CBA’s own cash-flow maths is sound, and its recovery does not rest on rents alone. It pays to run the numbers, because the recovery story stands or falls on them. We reproduced CBA’s estimate from its stated assumptions, and it holds: for a typical Sydney investment property bought with a 20% deposit, removing negative gearing is worth roughly $14,000 a year in lost tax benefit, equivalent to the mortgage rate rising about 1.4 percentage points. (CBA puts the range at 135 to 165 basis points, where 100 basis points is one percentage point, and our figure lands in the same range.) That covers the negative-gearing side only; the capital gains change is a separate cost, felt when the property is sold rather than in the yearly holding costs.

If rents had to do all the work at today’s price, our own calculation says Sydney’s gross yield would need to climb about 1.1 to 1.3 percentage points, from 3.2% to roughly 4.4%, to cancel the cash-flow hit in full. But CBA does not assume that. In its framework the yield only has to rise far enough to offset part of the higher holding cost, because owner-occupiers, who are untouched by the change, keep buying and support prices. The rest of the adjustment comes from the one-off price fall itself, and CBA expects lower interest rates in 2027 to help as well.

On the rent side, even an optimistic, quick-recovery view lifts the yield only about 0.4 of a percentage point, from 3.2% to about 3.6%. That is the bullish reading of how fast rents catch up, and it covers roughly a third of the full cash-flow hit. The point is not that the recovery fails. It is that rent cannot carry it alone at today’s price, so the rest comes through the one-off price reset CBA forecasts. The regime-change risk is that investors stay away even after prices have fallen, leaving growth permanently flatter.

One honest qualification, because it matters. CBA notes that investors can “quarantine” the lost deductions and carry them forward to offset future rental income or a future capital gain. So the full figure is the upfront cash-flow cost, not the permanent cost, and some of the benefit returns later. The real question is how much investors value a tax benefit they can no longer use to help pay this year’s holding costs. CBA’s own revision, lifting its long-run price drag from about 3% to just under 5%, reflects a judgement that they will not value it much. That judgement is exactly what the reset-versus-regime question turns on.

The supply floor the argument ignores

In the booming capitals, prices are holding up because demand still outstrips the supply of homes, and it is that imbalance that matters, not investor demand on its own. Perth, Brisbane and Adelaide have all seen population growth run ahead of new building for years, on CBA’s own read. Weaker investor sentiment does pull on demand there too, which is part of why momentum has eased. But with homes this scarce, losing some investor demand slows the pace rather than reversing it, so prices keep climbing. Rents tell the same story: house rents grew 6.3% in Brisbane and 6.1% in Perth over the year to February 2026, against just 0.9% in Melbourne. Rising rents in a tight market lift yields the slow way, by the rent going up rather than the price coming down.

That imbalance is the structural point our analysis keeps returning to. Australia added about 424,000 people in the year to September 2025. Where building has not kept up, homes are scarce relative to the people who want them, and that scarcity pushes prices and rents up. In the supply-short capitals that is the dominant force on prices, not the cash rate and not the tax treatment of investors. Our standing position is that interest rates are a weak predictor of prices over the long run. They still bite in the short term: the recent run of rate rises and softer confidence is pulling Sydney and Melbourne down now, and has slowed even Perth. Over the medium term, supply sets the floor that prices return to.

So the reset-versus-regime question, real as it is, mostly bites where investors are doing the heavy lifting. Where homes are genuinely scarce, weaker investor demand changes who buys more than what they pay: fewer investor purchases are largely taken up by owner-occupiers instead, as CBA itself notes.

The bottom line

Whether the Budget changes prove a one-off reset or a permanent downshift is a real and unresolved question, and it lands mainly where investors are concentrated and yields thin: Sydney most of all, and the investor end of Melbourne. But the reforms do not start until 2027 and leave today’s owners untouched, so the weakness already in Sydney and Melbourne is the rate-and-affordability cycle, not the tax change. The recovery does not rest on rents alone, which is why CBA still expects a one-off step-down rather than a permanent slide. For owners in the softer capitals the near-term path looks weaker than the flat national headline, while for buyers in the supply-short capitals the investor question is a sideshow, since the people-to-homes gap driving those markets has not changed.

Cut through the noise on Australian property

Subscribe for free.